Most firms in UK financial services can clearly describe what good customer outcomes should look like under Consumer Duty. They have defined vulnerable customer policies. They have value assessments. They have board reports referencing the four outcomes.

The difficulty is not designing the framework. It is operationalising it.

Far fewer firms can evidence outcomes in a way that is consistent, granular and defensible across their entire customer base. When asked to show how good outcomes are monitored in practice, many rely on samples, complaint data, attestations or periodic reviews. Those approaches feel structured. Under scrutiny, they often fall short.

Consumer Duty does not simply require firms to articulate standards. It requires them to demonstrate, with data and structured oversight, that those standards are being met continuously. The challenge is translating policy into interaction-level proof.

This guide explains what the FCA actually expects, what types of evidence hold up in a review, what commonly fails, and how to build an evidence framework that works in practice.

→ For a full overview of evidencing Consumer Duty at scale, see our guide: Consumer Duty Compliance Guide for UK Financial Services

What the FCA’s Consumer Duty Evidence Standard Actually Requires

The Consumer Duty was introduced through a document called PS22/9, which is the FCA’s final policy statement setting out the rules in full. Within it, the FCA requires firms to hold adequate data and management information to monitor whether they are achieving good outcomes for their customers.

That sentence is worth a deeper look. “Management information” means the data and reporting that firms use to understand what’s happening across their business. “Adequate” is the key word. The FCA has made clear, through its own supervisory reviews and published findings since the Duty came into force, that adequate doesn’t mean occasional. It doesn’t mean a sample. It means ongoing, systematic, and verifiable.

In practical terms, adequate oversight means being able to show a clear, documented chain from the policies a firm has in place all the way through to what customers actually experienced. If a firm states in its board report that it delivers fair value to customers, it needs evidence that supports that claim across the full range of relevant customer interactions, not just the small proportion it happened to review.

When the FCA visits a firm or requests information as part of a supervisory review, it is looking for four things: that the firm monitors its customer interactions continuously rather than occasionally, that it has insight into what is happening across all customers rather than a small sample, that it identifies problems before customers start complaining, and that its records are structured and retrievable rather than scattered and ad hoc. Firms that cannot demonstrate these things are not meeting the standard, regardless of how good their intentions are.

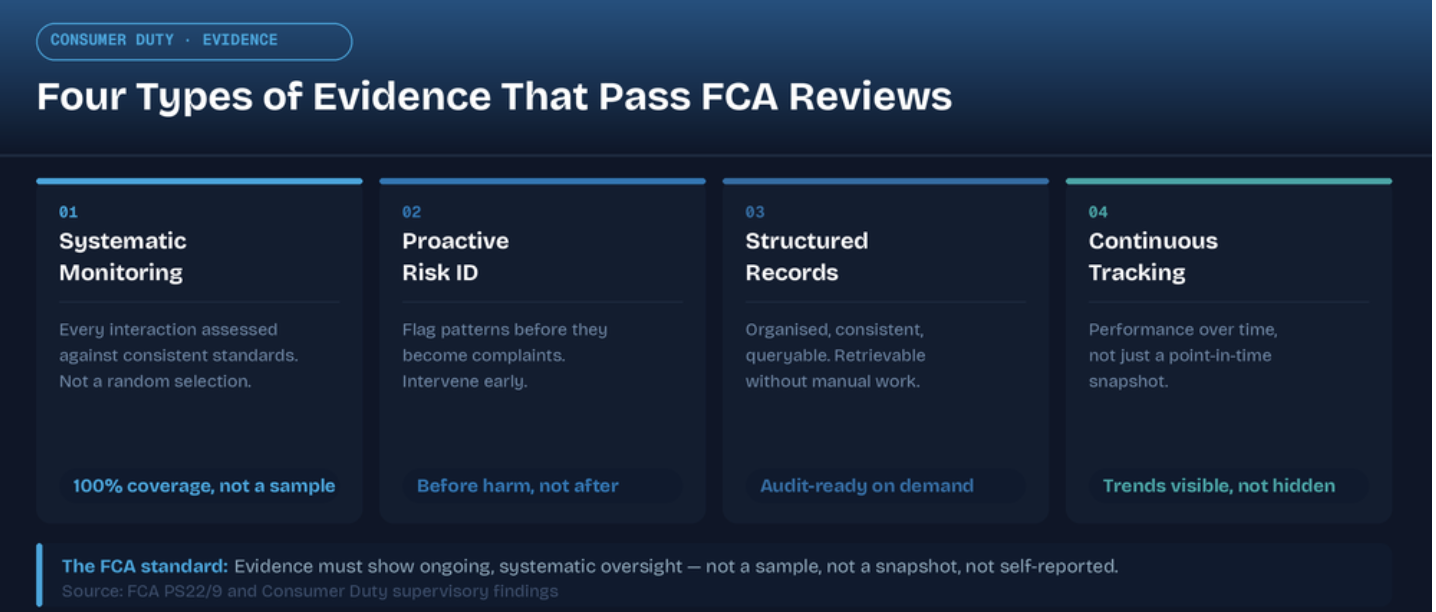

Four Types of Consumer Duty Evidence That Pass FCA Reviews

Systematic interaction monitoring across all customer interactions

When the FCA asks a firm to evidence good customer outcomes, it is asking about the whole picture, not a selected portion of it. Systematic monitoring means that every relevant customer interaction, whether that is a phone call, a meeting, or a digital exchange, is assessed against consistent standards, not just a random selection of them.

This matters because problems tend not to distribute themselves evenly. A customer who is vulnerable, confused, or being given unsuitable advice is not necessarily going to appear in a 5% sample. Systematic monitoring across all interactions means that when the FCA asks what is happening across the customer base, the firm can actually answer the question.

Proactive risk identification before complaints surface

A complaint is a customer telling a firm that something has already gone wrong. By the time a complaint arrives, the harm has occurred. The Consumer Duty expects firms to identify risks to customers earlier than that, before the customer has been harmed, not after.

Proactive risk identification means having monitoring systems that flag concerning patterns in customer interactions as they emerge, so that compliance and quality teams can investigate and intervene before an issue becomes a systemic problem or a regulatory one. Firms that rely on complaints to tell them where their risks are will always be responding to harm rather than preventing it.

Structured, searchable records that can be audited on demand

When an FCA supervisor requests evidence, they typically need it quickly and in a form that can be reviewed systematically. If a firm’s evidence exists as a collection of free-text notes, informal records, or information spread across multiple disconnected systems, it cannot be produced in that way.

Structured evidence means records that are organised, consistent, and queryable. A compliance team should be able to pull together documentation showing how a specific group of customers was treated during a given period without days of manual work. If they cannot, the evidence effectively does not exist in the way the regulator requires it to exist.

Outcome tracking that shows performance over time, not just at a point in time

A single review of customer outcomes, even a thorough one, only tells you what was happening at the moment the review took place. A firm that conducts a Consumer Duty assessment in January and then waits until the following January to look again has no idea whether outcomes improved, deteriorated, or changed shape entirely in the months between.

The FCA expects firms to track customer outcomes continuously, so they can identify trends, spot deterioration early, and demonstrate that they are responding to what the data shows. Ongoing tracking, consistently applied, is what separates a functioning oversight framework from a compliance exercise.

Five Consumer Duty Evidence Approaches the FCA Challenges When Used Alone

Sample-based monitoring covering 2–10% of interactions

Sampling, the practice of reviewing a small percentage of customer interactions and drawing conclusions about the whole, was an accepted approach under previous regulatory frameworks. Under Consumer Duty, it is no longer sufficient on its own.

The shift in expectation is significant. Consumer Duty expects firms to demonstrate consistent outcomes across every interaction, yet many still depend on systems that only review a small fraction of calls. Reviewing 2–10% of interactions tells a firm something about those interactions. It tells them very little about the rest. The FCA has previously called out the practice of merely re-packaging existing data as poor practice, making clear it expects firms to consider carefully whether the data they hold is genuinely sufficient for the customer outcome monitoring the Duty requires. A sample, however well constructed, cannot surface harm that occurred in the interactions it did not cover.

The FCA’s board report review identified a related issue. Many firms presented MI with pass or fail ratings but provided no reasoned explanation for why thresholds were set where they were. Without that rationale, boards cannot assess whether the boundary between good and poor outcomes is reasonable. A sample that produces a high pass rate is not evidence of good outcomes if the firm cannot explain what a pass actually means.

Complaint data used as a proxy for fair outcomes

A low complaint rate feels like a positive signal. In reality, it is a limited one. Research consistently shows that the majority of customers who experience poor service or unfair treatment do not complain formally. They leave quietly, accept the outcome, or do not realise they had grounds to raise a concern.

Using complaint volumes as the primary measure of customer outcomes means a firm only ever learns about the problems its customers chose to report. Under Consumer Duty, firms are expected to identify harm proactively, meaning they need evidence of what is actually happening across all customer interactions, not just a record of who complained about it.

Unstructured notes that cannot be systematically reviewed

Many firms hold a significant amount of information about customer interactions in the form of adviser notes, contact centre records, and case management comments. The problem is that free-text, unstructured records cannot be systematically analysed. An FCA supervisor cannot draw conclusions from hundreds of individually written notes that cannot be queried or compared across teams and time periods.

For evidence to be useful under Consumer Duty, it needs to be reviewable at scale. If extracting meaningful insight from a firm’s interaction records requires a team of people manually reading through documents for weeks, the evidence is not functioning in the way the regulator expects.

Adviser attestations with no independent verification

An attestation is a formal statement, usually signed, in which a member of staff confirms they have followed the required process. Attestations have a legitimate role in compliance frameworks, but they cannot stand alone as evidence that customers received good outcomes.

The reason is straightforward. An attestation tells a firm what an adviser says they did. It does not verify what actually happened in the customer interaction. Under Consumer Duty, the expectation is that firms independently verify that customers are being treated well, not that they take staff confirmation as sufficient proof. Without supporting interaction-level evidence, an attestation leaves a significant gap.

Annual assessments with no ongoing monitoring between them

A structured annual Consumer Duty assessment is a useful exercise, but it is not a substitute for continuous oversight. Conducting a thorough review in March tells a firm what was happening in March. It says nothing about April through February.

The Consumer Duty standard requires firms to maintain ongoing awareness of how their customers are being treated. An annual assessment cycle with no active monitoring in between means a firm has no way of knowing whether its outcomes have changed, whether new risks have emerged, or whether an intervention it made actually worked. By the time the next annual review comes around, a great deal could have gone wrong in the interim.

If any of those five approaches sound familiar, you are not alone. The gap between what firms assume is sufficient and what the FCA actually expects is wider than most realise. Our guide to evidencing Consumer Duty at scale covers what closing that gap looks like in practice: Consumer Duty Compliance Guide for UK Financial Services

What Firms Thought Was Adequate Evidence (and Why It Wasn’t)

The following are illustrative scenarios based on the types of compliance gaps commonly identified in Consumer Duty reviews. They’re examples, not verified case studies.

Illustrative example: good sample results, incomplete picture. A firm conducts monthly quality assurance reviews covering approximately 5% of adviser-client interactions. Reviewers find an acceptable pass rate and report this to senior management. When an FCA supervisor asks for evidence that vulnerable customers are receiving fair treatment across all customer interactions, the firm cannot produce it. The 5% sample contained no flagged vulnerability indicators, but the other 95% had never been reviewed. The firm considered the sample representative. The FCA found the evidential basis inadequate.

Illustrative example: complaint statistics presented as compliance evidence. A firm’s Consumer Duty submission includes complaint statistics showing a low complaint rate, signed adviser attestations confirming that suitability processes were followed, and a point-in-time outcome review carried out six months earlier. When the FCA asks how the firm monitors ongoing customer outcomes across different segments and channels, the firm has no continuous monitoring data. Low complaint volumes did not demonstrate fair outcomes. They demonstrated that customers had not formally raised concerns. The gap between what the firm believed was evidence and what the FCA required was substantial.

Illustrative example: policy without proof of practice. A firm produces detailed policies for identifying and supporting vulnerable customers, defined by the FCA as people who, due to their personal circumstances, are especially susceptible to harm. When asked to demonstrate how those policies translate into consistent day-to-day practice, the firm presents written guidance and training records. It cannot show interaction-level data demonstrating whether customers who displayed vulnerability indicators actually received appropriate support. The policy existed. The proof that it was consistently applied did not.

Illustrative example: MI that contradicted the conclusion. A firm produced a detailed description of its work to support customers with characteristics of vulnerability, covering policies, training, and staff initiatives. The accompanying MI showed that fewer than half of customers in that group were receiving good outcomes. The FCA found the report internally inconsistent. The narrative claimed compliance while the data showed something different. Firms should ensure conclusions are directly supported by the MI presented, not asserted alongside it.

What Adequate vs. Inadequate Consumer Duty Evidence Looks Like Across the Four Outcomes

The Consumer Duty is structured around four specific outcomes that every regulated firm must be able to evidence. These are: products and services, price and value, consumer understanding, and consumer support. Each one carries distinct evidential requirements.

Products and services. Adequate evidence shows systematic, ongoing monitoring of whether products are consistently explained and promoted in ways that match the characteristics and needs of the intended customer base. Inadequate evidence is product approval documentation created at launch, with no ongoing monitoring of how products are actually presented in customer interactions after the fact.

Price and value. Adequate evidence demonstrates continuous monitoring of whether customers are receiving fair value, including the ability to identify customers who may be paying for products that do not suit their circumstances. Inadequate evidence is a pricing justification written when the product was designed, with no subsequent tracking of whether customers’ real-world experience of value aligns with what was intended.

Consumer understanding. Adequate evidence demonstrates, through systematic analysis of actual customer interactions, that customers across different segments genuinely understand the information they receive. Inadequate evidence is a readability score applied to written communications, with no monitoring of whether information is being clearly communicated in the conversations that actually shape customer decisions.

The FCA found that some firms reviewed hundreds of communications and reported high completion rates, but could not demonstrate that customers had actually understood the information. Reviewing and approving a communication is not the same as evidencing comprehension. Adequate evidence connects the content of communications to how customers responded to them, whether through feedback, behavioural data, or interaction monitoring.

Consumer support. Adequate evidence shows that customers receive support appropriate to their individual needs, with systematic identification of vulnerability indicators and consistent application of suitable responses. Inadequate evidence is a vulnerability policy and a signed attestation that the policy was followed, without interaction-level data to back it up.

How to Structure Consumer Duty Evidence That Holds Up to FCA Scrutiny

Firms that build Consumer Duty evidence frameworks that hold up under regulatory scrutiny tend to share several structural characteristics. Their monitoring runs continuously rather than in periodic bursts. Their evidence is built from the interaction level upwards, aggregated into meaningful trends rather than derived from sample extrapolation. Their records are structured so they can be retrieved and presented systematically when the regulator asks for them. And their evidence framework creates a clear, traceable chain from policy through to practice through to outcome.

For most firms, reaching that standard manually is not realistic. The volume of customer interactions across a typical financial services business means comprehensive human review of every interaction is not feasible. This is where automated monitoring tools, which can analyse 100% of relevant customer interactions, flag risk indicators consistently, and generate structured and retrievable records, make the difference between having an evidence framework that works and one that only appears to.

The question every compliance officer and quality assurance leader should put to their current approach is not whether it looks like adequate evidence. It is whether it would hold up when an FCA supervisor looks closely at it. For many firms, that is a different question with a different answer.

Want the full framework for building Consumer Duty evidence that holds up to FCA scrutiny?

Start here: